Public Ruling Capital Allowance

Capital Allowances Expense Tax Deduction

Public Ruling Irb Capital Allowances Accountancy He02 Studocu

Inland Revenue Board Of Malaysia Qualifying Expenditure And Computation Of Capital Allowances Public Ruling No 6 Pdf Free Download

Accelerated Capital Allowance Chartered Tax Institute Of Malaysia

Http Www Hasil Gov My Pdf Pdfam Pr 12 2014 Pdf

Http Www Hasil Gov My Pdf Pdfam Pr 10 2012 Pdf

Claiming allowances public ruling no.

Public ruling capital allowance. Qualifying expenditure 2 7. It explains the tax treatment of accelerated capital allowances for plant and machinery under various gazette orders which are in force and gazetted up to 2017. Procedure for claiming capital allowances 28 director general s public ruling section 138a of the income tax act 1967 ita provides that director general is empowered to make a public ruling in relation to the application of any provisions of ita. Relevant provisions of the law.

Special rates of allowances special rates of allowances provided under schedule 3 of ita 1967 and income tax rules may be categorized to accelerated capital. A public ruling is published as a guide for the public and officers of the inland. 31 december 2014 page 1 of 12 1. Letting of part of building used in the business 28.

Relevant provisions of the law 1 3. 2 2017 date of publication. 12 2014 date of publication. And b computation of capital allowances for expenditure on plant and machinery.

The objective of this public ruling pr is to explain a tax treatment in relation to qualifying expenditure on plant and machinery for the purpose of claiming capital allowances. Income tax rules 2 8. Objective the objective of this public ruling pr is to explain a whether the qualifying expenditure qe incurred by a person on the purchase or acquisition of capital assets for the purpose of claiming. It sets out the interpretation of the director general in respect of the particular tax law and the policy as well as the procedure applicable to it.

Application of the law 1 5. Replacement cost of furnishings 28 13. 8 oktober 2018 contents page 1. Capital allowance 25 11.

Public ruling 7 2018 accelerated capital allowance is an updated second edition of public ruling 4 2013 accelerated capital allowance. 15 april 2013 page 5 of 34 forest allowance roads and buildings for timber extraction 10 living accommodation for workers 20 7. Steps to claim accelerated capital allowance 11. A ruling is issued for the purpose of providing guidance for the public and officers of the inland revenue board of malaysia.

7 2018 date of publication. Accelerate capital allowance public ruling no. A public ruling is published as a guide for the public and officers of the inland revenue board of malaysia. It sets out the interpretation of the director general of inland revenue in respect of the particular tax law and the policy and procedure that are to be applied.

Objective the objective of this public ruling pr is to explain whether an asset is a qualifying plant and machinery for the purpose of claiming capital allowances in determining the statutory income from a business. It sets out the interpretation of the director general of. A public ruling is published as a guide for the public and officers of the inland revenue board of malaysia. Claiming capital allowances public ruling no.

Industrial building allowance 28 12.

Inland Revenue Board Of Malaysia Ownership And Use Of Asset For The Purpose Of Claiming Capital Allowances Public Ruling No Pdf Free Download

Http Www Hasil Gov My Pdf Pdfam Pr 5 2014 Pdf

Inland Revenue Board Of Malaysia Ownership And Use Of Pdf Free Download

Public Ruling Irb Capital Allowances Accountancy He02 Studocu

Inland Revenue Board Of Malaysia Qualifying Plant Inland Revenue Board Of Malaysia Qualifying Plant Pdf Pdf4pro

Inland Revenue Board Of Malaysia Ownership And Use Of Asset For The Purpose Of Claiming Capital Allowances Public Ruling No Pdf Free Download

Pdf Capital Allowances For Depreciating Assets A Successful Reform

Http Www Hasil Gov My Pdf Pdfam Pr 2 2017 Pdf

Taxavvy Issue 9 2018

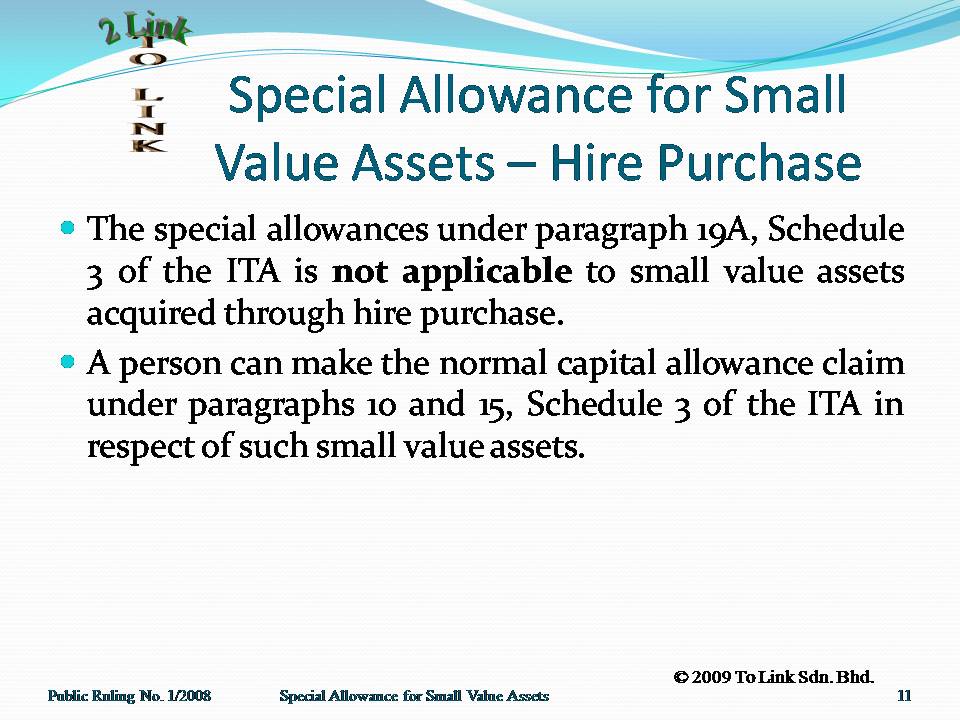

Special Allowance For Small Value Assets Small Value Assets Slide No 11

Http Www Ctim Org My File News 50 03003 E Ctim 20tech Dt 2012 2015 20 20public 20ruling 20no 2012 2014 20 20quaifying 20plant 20and 20machinery 20for 20claiming 20capital 20allowances Pdf

Special Allowance For Small Value Assets Small Value Assets Slide No 06

Lhdn Latest Tax Case Bcsb Vs Ketua St Partners Plt Chartered Accountants Malaysia Facebook

.jpg)